This is about donating to DAFs, Family Foundations and Charity. In December, it is common for people, particularly investors and business owners, to take stock of their successes for the year (as well as failures) and try to think of the best they can do with both of those things, tax-wise. Gains are wonderful, but they have costs associated with them. You don’t like losses, but you may be able to leverage them. All this is why you go to a CPA and not the reason you are reading this post.

This is about donating to DAFs, Family Foundations and Charity. In December, it is common for people, particularly investors and business owners, to take stock of their successes for the year (as well as failures) and try to think of the best they can do with both of those things, tax-wise. Gains are wonderful, but they have costs associated with them. You don’t like losses, but you may be able to leverage them. All this is why you go to a CPA and not the reason you are reading this post.

This post is about this question: What if I have money I want to give to charity (and I have some sort of a deadline to do it), but I want to figure out where I want to donate later?

I have addressed Islamic Charitable Planning before- how to give over the long term, including devices like charitable remainder trusts and charitable lead trusts (which come in a vast array of permutations). These generate tax benefits and philanthropic contributions that a donor must give to charity, a term we now need to define. But what if the “charity” you donated to was not necessarily a charity that did anything charitable itself. It was just a “charity holding” entity that sat on the money until you figured out what you wanted to do with it?

For Muslims, a Family Foundation or a Donor Advised Fund can function as a large version of a “Sadaqa Jar” parents keep at home to teach their children about giving. It’s money earmarked for charity, but it’s not charity until someone picks up the jar and takes it to a charity. The difference here is that the person giving in charity has already notified the IRS and obtained tax benefits for giving in charity without necessarily parting with the money.

Why Sit on Charitable Dollars?

For those aware of vast unmet human needs worldwide, the notion that billions in charitable dollars (that people received tax benefits for giving away) are just sitting there can be offensive. The practice of donors sitting on “donations” has been controversial for some time. Sometimes donors have no real desire to do anything with the money (or stocks or real estate) they “donated,” though this is not always the case. Often there is a plan.

In reality, there are two reasons for what may appear to some (and in many cases is) hoarding of financial assets for charity. The first is perhaps a result of an awful federal tax policy that encourages hoarding dollars for “charity” among people who are scarcely interested in charity at all. You may remember this problem from news about the Trump Foundation. Yes, they broke laws and were never a legitimate charity, but you can get away with a whole lot of morally questionable behavior in family foundations without breaking any rules.

The second reason is when people create a charitable plan for their family, but they are not interested in giving all their money to a specific charity right this minute. There are good reasons for this.

Why Not Just Give all Charitable Dollars to Actual Charities

Here is a hypothetical: Last year, Saleema wanted to give $5,000 to a charity for the poor. That amount counts as her Zakat. Saleema researches a local Zakat committee at her Masjid that distributes funds to those locally in the most need. The masjid committee gives the money way rapidly.

This year, shares Saleema owns in a privately held company were purchased by a large company, providing her and her family with a massive windfall. She wants to give $50 million to charity, about a quarter of her net worth. Now Saleema likes and has donated to many charities over the years. Saleema does not like any of these charities so much that she will give them $50,000,000 right away.

Saleema wants a plan. She wants to make meaning and have her dollars count in the best possible way. Her head is spinning with the blessings she has and the possibilities for good. She also knows that giving large amounts of money to a specific nonprofit can be wasteful, and she may end up regretting it. If you give a charity $5,000, they will put it to good use. Give them $50,000,000, and the board of directors might go on an irrational spending spree. Waste has happened many times before. They may place the funds in an endowment, but this does not solve the hoarding concern. She wants to put the money to good use, not necessarily just have generated fees for a sizeable hedge fund.

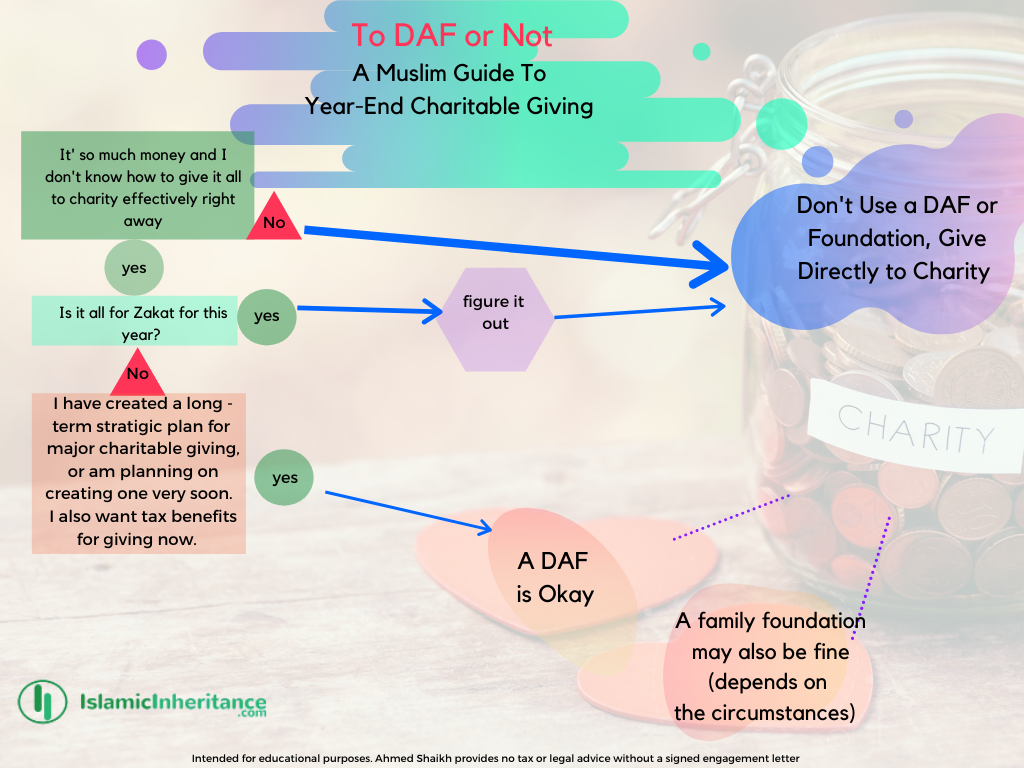

Saleema must now decide between a Charitable Family Foundation or a Donor Advised Fund.

Sadaqa Jar Giving: Family Foundations

No matter what Saleema decides on, she has to consider overhead- funds spent on things that do not benefit the charitable mission directly but are still necessary (though this is sometimes debatable). If you just give to a charity, there is overhead associated with charitable giving. But both Donor Advised Funds, and Family Foundations generally don’t have philanthropic projects. They typically provide grants to other charities. There are exceptions to this, of course. Both DAFs and Family Foundations routinely offer scholarships (which is a grant).

Saleema could select a Family Foundation, which is a private charity that can include her and her family members as board members. These are regulated more stringently by the IRS, and the tax benefits may not be as great for some people. But in this example, for Saleema, the tax benefits with a family foundation are adequate. The problem is the maze of rules and reporting and a regime of excise taxes and bad behavior penalties. However, there are many benefits to having your family control these funds, including getting the next generation or two more deeply involved in philanthropy.

Some Grantmakers like to use funds for studies. Donors may want to provide potable water to a poor Bangladeshi village, increase literacy, develop small businesses. There may be lots of ways to do any of these things. Some may be effective; others are wasteful or even harmful to the people you are trying to help. There may be professionals that will allow donors (who still have control of the funds) to know the difference. They can then create a plan and carry it out.

Some charities create a foundation designed to continue in perpetuity because they want to award grants and scholarships. They want successive generations of family members involved in the giving process.

Donor Advised Funds (DAFs)

A Donor Advised Fund (DAF) is very similar to a private foundation, only it’s a separate fund inside an entity organized as a public charity. Think of it as an account in a bank or brokerage (and a DAF is often no more than that). They are common in “community foundations” that direct philanthropy in a local or regional setting. The largest institution that provides DAF is Fidelity, which integrates the service with its online brokerage; other online brokerages do the same thing now. There are faith-based community foundations as well, and many of them are enormous. There is a “American Muslim Community Foundation” in the San Francisco Bay Area (look for my review at the Ehsan Newsletter which is not out yet).

DAFs combine most of the advantages of a Family Foundation without as much of the cost. The government has rules in Private Foundations that prevent (in a limited way) hoarding that are not present in public charities. They do have overhead associated with them, but it’s relatively small.

Saleema can, if she wants to, donate all of her stock to the DAF, get a massive tax deduction. She can also not give any of the money to actual charities that do charitable work until she is good and ready. The Donor Advised Fund will charge her for their overhead (a percentage of the amount in her account), and there will also be a charge for an investment advisor, but she has immense flexibility when it comes to how she will donate.

Or Just Start an Actual Charity

Another possibility is that she creates a “public charity” -the kind you have probably donated to many times, not tied to a specific family. Creating a new charity could be significant. It can also be a trap. The main goal of virtually any charitable institution is often not the charitable work it does, but to sustain the institution itself. A self-eating ice cream cone. Institutions perpetuating themselves is acceptable to a point though.

Donors create Universities and hospitals, but in the United States, many have questionable charitable value. Some notable philanthropists have avoided this by deciding to give away all their money during a defined period. Their work may continue through the initiatives they started, and the lives their work may have saved, but the charity created to distribute the money will be gone.

Use of Zakat

With a Foundation or DAF, you have not given anything no matter what your tax return says. In fact, in many ways, it can continue to benefit you. A business owner may transfer the business stock into a family foundation but continue to use those shares to maintain majority control of the business. This happened in “Batman Begins” if you happened to see that movie, (“look, it’s all a bit technical”).

If you have any current Zakat due (like when you calculate it at the end of the calendar year or during Ramadan), don’t donate it to a DAF or a Family Foundation. Give it away so that it would benefit those who need it as soon as possible. Donating to a DAF, then directing the DAF to contribute to an actual charity that does charitable things is wasteful as you are subjecting your dollars to needless overhead.

However, you may use these funds (and those in other forms of Islamic Charitable Planning) for a fund from which you pay your Zakat annually.

When To Use Charitable Planning

I created a chart describing when you should just donate to a Charity and when it may make sense to give to a DAF or create a private foundation.

P.S.

To schedule a 15-minute mini-consultation on Islamic Estate Planning, you should click on my calendar link.

Forward or share this article if you found it useful .