Baitul Maal is the Islamic treasury, and in some cases it can receive a person’s inheritance. For the past couple of decades, I have worked on Islamic estate plans for thousands of clients. Usually, inheritance goes to family members: parents, a spouse, children, siblings, or extended family. In other words, there is usually someone—provided those relatives are:

- Alive

- Muslim

You would think people would know whether they have relatives entitled to inherit. Not always. I am dealing with a public case right now where a man died alone at home, and his family did not learn of his death for more than six months. His body remained in a hospital freezer during that time. There was no janazah. Eventually, I did what I could to help him get one, including recruiting family members he had never met. He had many relatives, but he was not in touch with them. They were disconnected. He died intestate, meaning he had no will, living trust, or instructions for what should happen after death. In that situation, Islamic inheritance rules did not control. The state’s intestacy statute did.

Families become disconnected for many reasons: ordinary conflict, meanness, or traumatic historical events such as the Partition of South Asia. It happens more often than many people realize.

Still, if heirs exist, the estate administrator must find them. If they are not found, the estate may ultimately go to the state.

Another scenario involves Muslims who came to Islam later in life. They may not have a Muslim spouse, parent, sibling, or child. They may have adult children raised outside Islam. That creates complexity. Based on a hadith, a non-Muslim cannot inherit from a Muslim. So non-Muslim relatives do not inherit as Islamic heirs. They can, however, receive assets through the wasiyyah—the one-third discretionary amount given outside the fixed inheritance shares.

What happens to the other two-thirds?

The answer resembles what happens when someone dies without a will in a state like California: the intestacy statute controls. In Islamic inheritance, however, the concept has broader application. The remaining property may go to Baitul Maal. But because there has been no khilafah for the past century, no centralized treasury exists in the traditional sense.

Let’s walk through calculation a bit

Calculating Inheritance

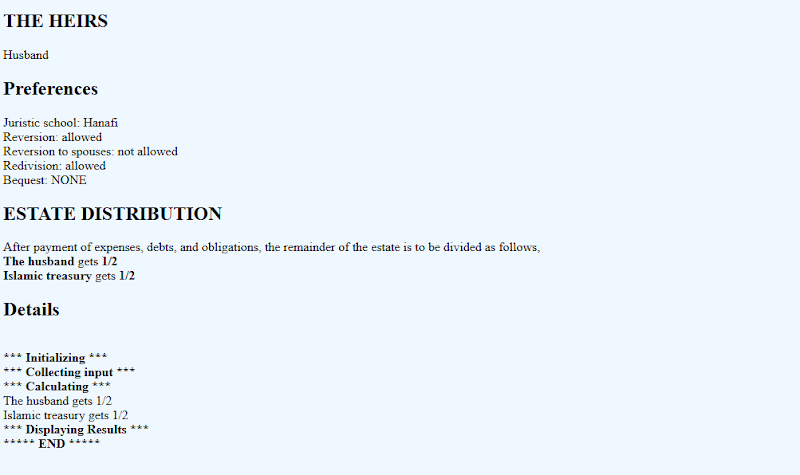

If you were to go to a calculator like islamicsoftware.org/irth, using the Hanafi madhab (which my writing tends to default to) and say someone like Sally has no Muslim family members, except for a husband, the shares would look like this:

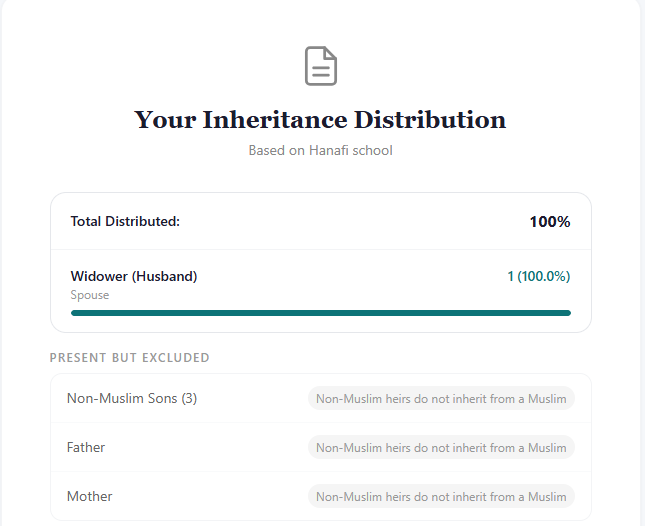

While any Islamic Inheritance Calculator can make mistakes, including my own, this one is not wrong. Baitul Maal gets 50%. However, in my own calculator, I do it a bit differently. So the calculator at islamicinheritance.com/calculator give it to the only heir.

In the islamicinheritance.com calculator, we have everything going to the husband. This is not the actual rule in any school of fiqh. It’s just what we do because we don’t have much choice. In the absence of any such thing as “Baitul Maal” we will make sure distribution takes place to the only heir there is. In this case, a husband. Now note I have non-Muslim sons and non-Muslim parents in this situation. The wasiyyah is available as a planning tool for this person as I discuss below. But there are more options than that.

In planning, there are a few options:

1. There is one heir.

Sally is 63. She became Muslim two years ago and married Bilal last year. She has three adult children, none of whom are Muslim. She loves them and wants them to receive her estate after she dies.

Sally has options. Traditionally, under various schools of thought, Bilal receives only half of her estate. Because no other eligible heirs exist, the rest would go to the Baitul Maal. Since no such thing exists in the traditional sense, I would plan for Bilal to receive it all. That part is clear, but what about the children?

But Sally also wants to benefit her children. At death, she is limited to the one-third wasiyyah. During life, she can make gifts, including through an irrevocable gifting trust that may protect her children from risks such as bankruptcy, divorce, and other financial hazards.

2. There are no heirs at all.

Suppose Sally never marries Bilal. She can still give up to one-third of her estate through a wasiyyah and make lifetime gifts. But assets still in her name at death must go somewhere. One common option is charity. She can name a charity she likes and treat it as serving a role similar to Baitul Maal for planning purposes. There is an actual charity—one I have a rather dim opinion of, but a charity nonetheless—that uses this name. The point is simple: name the charity.

Being Creative

Another option is a trust that does more than an existing charity would. It may require more administration, but it can be a creative and useful way to use the funds. It may also benefit non-Muslim relatives without making the transfer “inheritance.”

For example, the trust could fund scholarships or provide financial assistance to future descendants facing unemployment or hardship.

Baitul Maal does not arise in most estate plans. But if you do this work long enough, you will see it. Another important part of any Islamic Estate Planning is to understand that there is a need to be flexible, creative and adapt to the circumstances we have now.

If you want to discuss Islamic Estate Planning for your family with Islamic Estate Planning expert Ahmed Shaikh, be sure and reach out for a 15-minute no-obligation zoom meeting.

Say you are in a crowd of people: Look to your left. Then look to your right. Chances are high that one or both of those people is going to be cremated. If you are Muslim and you are in a crowd of Muslims, then that statement is not true (I hope).

Say you are in a crowd of people: Look to your left. Then look to your right. Chances are high that one or both of those people is going to be cremated. If you are Muslim and you are in a crowd of Muslims, then that statement is not true (I hope). Do you want to donate your body for the purpose of having scientists, medical students and potentially others dissect it? Do you want to have your body chemically treated to be placed in museum displays? How about displayed in private collections? The Islamic Medical Association of North America has taken the position

Do you want to donate your body for the purpose of having scientists, medical students and potentially others dissect it? Do you want to have your body chemically treated to be placed in museum displays? How about displayed in private collections? The Islamic Medical Association of North America has taken the position