“Children are the enemy.”

I remember once many years ago attending a mandatory continuing legal education program (it is the kind of thing lawyers need to do) when an attorney talked about the relationship between his clients and their adult children.

Adult children are frequently stereotyped as greedy, manipulative, lacking in any real loyalty, love, and sense of duty. In some ways, this goes along well with my narrative about the breakdown of the American family. With this breakdown, there is a potentially exploitative system of taking care of the elderly. It is a system that strips them of their wealth, robs them of their freedom, alienates them from their family and drugs them into a stupor

The Netflix movie, “I care a lot,” has aspects of it that are incredibly frightening primarily because they happen. It is a movie, though, and so it is sensationalized. The Adult Protective system, as depicted in the movie, doctors, professional court-appointed fiduciaries, nursing homes, and others take advantage of the breakdown in the American family and profit from it together. Of course, there are going to be lawyers that are going to point out things and statutes in specific law and say, “well, that’s not exactly how it works.” While it is true that this is a movie that takes liberties, the actual abuse it depicts is accurate. Naturally, this is not the only aspect of American society where corruption exists.

It is not my place to deny that there is a need for a system to take care of those who cannot take care of themselves because people can be exploited, even by members of their own family. The cure, however, can be worse than the disease.

What the system is really like

My law practice is in California. Naturally, my description of what the system is like is going to center around the state. Should note that the systems in other states are generally similar though there may be essential differences from one place to another. There might even be changes in terminology.

Conservatorship

There are two different kinds of conservatorships in California. The first is a “Probate Conservatorship,” governed by the California probate code. Another is an “LPS conservatorship”- for the “gravely” disabled.

A judge supervises the powers of a conservator. These powers can be somewhat limited or can be incredibly draconian and comprehensive. It can easily include managing finances (probably the most common), relationships, medical treatment, and care-indeed, virtually absolute control.

Conservatorships are not a service provided by the government, not usually. They are mandated by the government and can look like a transfer of wealth from families to a privately-run system. The Ward, the person who has lost her freedom, pays for it, sometimes with everything she has- her wealth, liberty, even her dignity. One of the problems with creating any system like this is that the system will benefit itself more than the people the system is supposed to help. It is, of course, expensive for practical reasons as well; imagine having to hire somebody to manage your entire life?

As a practical matter, this system is not for the benefit of adult family members, particularly adult children. Adult children, of course, may become conservators themselves, in a process supervised by the courts. Much of the system will assume that adult children are the enemy, while professionals who are regularly in court and everyone else in the system are essentially public servants.

A way out of this nightmare

Some in this world can tell jokes, walk and talk, and may even be wise-the kind of people that you might go and ask for advice. Yet, conmen and women and random emails can exploit them relatively easily. The solution is depressingly simple: you need a plan.

An abusive system railroading an elder is more problematic for those who have a plan, which might include a revocable living trust and a power of attorney. You also need a process to determine whether you are incapacitated.

Three kinds of people

There are three different kinds of people in this world. There are the people that you trust, the people that you don’t trust, and then they’re the ones you don’t know. Now, of course, the people that you trust might include your family members or your friends. There may be family members you do not trust.

You, of course, have absolutely no idea about the motivations of individual judges, professional fiduciaries, nursing home managers, and others in the system. You don’t know if they are people of goodwill or ill will. You should also not want to find out.

Having a plan, including one that incorporates the Islamic rules of inheritance and the potential for your incapacity, is a great way to start. This includes an incapacity plan, a living trust and a power of attorney. It is your plan- because if you don’t get one yourself, the government has one for you.

PS To schedule a no-obligation 15-minute zoom call to go over the estate planning process, click here.

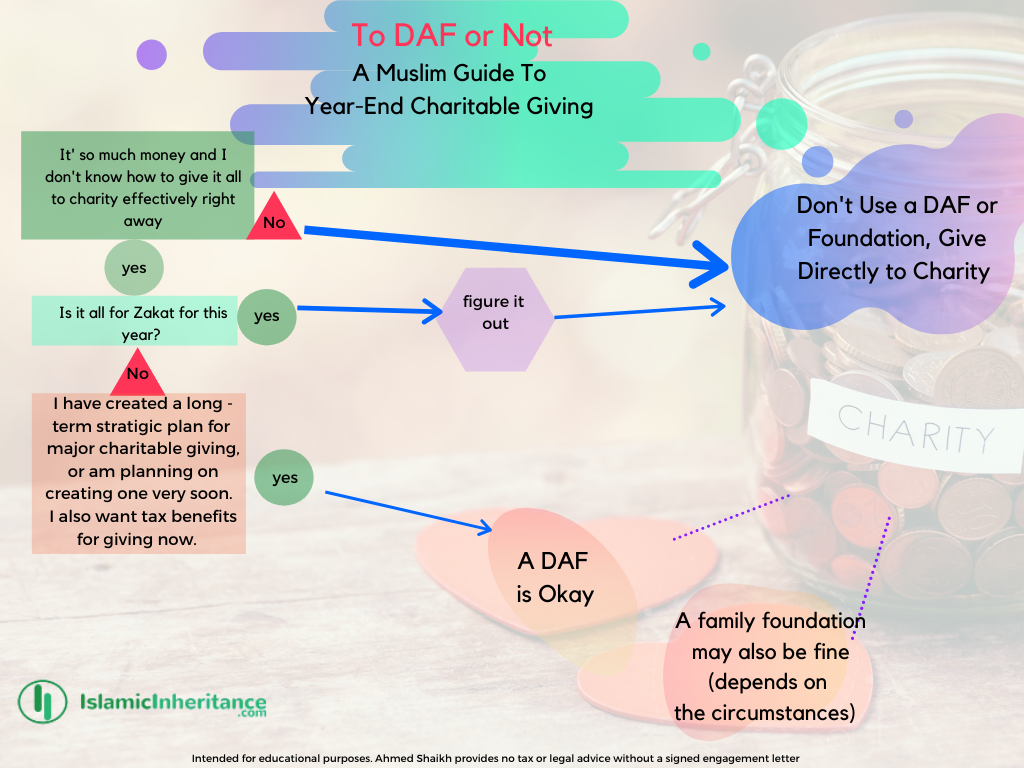

PPS American Muslim Community Foundation

I recently wrote about the concept of a “donor-advised fund.” In my Muslim nonprofit newsletter, which you can subscribe to here, I reviewed an organization that does Donor Advised Funds, the American Muslim community foundation (AMCF). While the organization has some promise, I found some serious problems, including with their Zakat policy. You can read about it here.

This is about donating to DAFs, Family Foundations and Charity. In December, it is common for people, particularly investors and business owners, to take stock of their successes for the year (as well as failures) and try to think of the best they can do with both of those things, tax-wise. Gains are wonderful, but they have costs associated with them. You don’t like losses, but you may be able to leverage them. All this is why you go to a CPA and not the reason you are reading this post.

This is about donating to DAFs, Family Foundations and Charity. In December, it is common for people, particularly investors and business owners, to take stock of their successes for the year (as well as failures) and try to think of the best they can do with both of those things, tax-wise. Gains are wonderful, but they have costs associated with them. You don’t like losses, but you may be able to leverage them. All this is why you go to a CPA and not the reason you are reading this post.

This email list is dedicated to

This email list is dedicated to